{kind=link}

When it comes to safeguarding your home, few risks feel as unsettling as flooding. It’s not only the immediate destruction that worries homeowners—the real concern often lies in the long-term financial burden left behind. At the heart of that financial impact are FEMA flood map zoning changes.

These updates may seem purely administrative, but their effects can be significant. A single change in flood zone classification can cause flood insurance premiums to jump sharply—sometimes adding thousands of dollars to your yearly costs. The good news? Homeowners are not completely at the mercy of these changes. By understanding how FEMA flood maps work and knowing how to respond, you can protect both your property and your finances.

Understanding FEMA Flood Map Zoning Changes

The Federal Emergency Management Agency (FEMA) develops and maintains flood maps for communities across the United States. Known officially as Flood Insurance Rate Maps (FIRMs), these maps define areas based on their level of flood risk and play a major role in determining flood insurance requirements and pricing.

However, these maps are not fixed. FEMA regularly updates them to account for new data, environmental changes, urban development, and advances in mapping technology. As a result, a property’s flood risk designation today may be very different from what it was just a few years ago.

Why does this matter? Because FEMA flood map zoning changes directly affect your home’s official flood risk classification—and ultimately how much you pay for flood insurance.

“Flood maps are living documents,” says Sarah Martinez, a flood insurance specialist with more than 15 years of experience. “Changes in climate patterns, land development, and improved data collection can all reshape flood risk assessments over time.”

FEMA Flood Zones Explained

FEMA assigns flood zones using a letter-based system to indicate varying levels of flood risk:

- Zone X (formerly Zones B and C): Areas with minimal to moderate flood risk

- Zone A: High-risk areas with a 1% annual chance of flooding

- Zone AE: High-risk areas where base flood elevations have been established

- Zone V: Coastal high-risk zones with added dangers from storm-driven waves

- Zone VE: Coastal high-risk zones with determined base flood elevations

When FEMA flood map zoning changes occur, properties may be reassigned to different zones. In many cases, homes are moved into higher-risk categories, triggering mandatory flood insurance requirements and leading to higher premiums.

How New FEMA Maps Directly Impact Your Premium

The connection between FEMA flood map zoning changes and your wallet is direct and significant. When your property moves from a lower-risk to a higher-risk zone, your premium doesn’t just increase incrementally—it can multiply.

Consider this reality: according to recent NFIP data, the average annual premium difference between a moderate-risk Zone X property and a high-risk Zone AE property is over $1,450. That’s not a small adjustment to your household budget.

The following table illustrates the dramatic impact of FEMA flood map zoning changes on insurance costs:

| Flood Zone | Description | Previous Average Annual Premium | Current Average Annual Premium | % Change |

| Zone X | Minimal flood risk areas | $575 | $650 | +13.0% |

| Zone B & C | Moderate flood risk areas | $895 | $1,050 | +17.3% |

| Zone A | High risk – no base flood elevation determined | $1,350 | $1,725 | +27.8% |

| Zone AE | High risk – base flood elevation determined | $1,650 | $2,100 | +27.3% |

| Zone V | Coastal high-risk areas | $4,200 | $5,850 | +39.3% |

| Zone VE | Coastal high-risk with additional hazards | $5,100 | $7,250 | +42.2% |

Source: National Flood Insurance Program (NFIP) Rate Analysis, 2024

These increases aren’t just theoretical. Take the case of the Johnsons in Florida, whose property was remapped from Zone X to Zone AE. Their annual premium jumped from $650 to over $2,000—a 207% increase that arrived without warning when their policy renewed.

But it’s not just the zone that matters. FEMA’s Risk Rating 2.0, implemented in 2021, introduced a more nuanced approach to calculating premiums. This system considers factors beyond just flood zones, including:

- Distance to water source

- Property elevation

- Foundation type

- First floor height

- Replacement cost

- Prior flood claims

Think of FEMA flood map zoning changes as the first domino in a complex chain reaction that ultimately determines your premium. The zone establishes your baseline risk, while these other factors fine-tune the final number.

7 Powerful Ways to Protect Your Premium

When FEMA flood map zoning changes affect your property, you’re not without options. Here are seven proven strategies to protect your premium:

1. Obtain an Elevation Certificate

An elevation certificate is like your property’s flood resume—it documents exactly how your structure sits relative to potential flood levels. This technical document, prepared by a licensed surveyor, can be your most powerful tool when FEMA flood map zoning changes occur.

Why? Because sometimes the maps are wrong. FEMA’s mapping technology has improved dramatically, but it still can’t capture every nuance of your property’s elevation. An elevation certificate provides the hard data that might prove your home sits higher than FEMA’s maps suggest.

Even if the zone designation is accurate, the certificate can help insurers calculate a more precise (and often lower) premium by documenting exactly how high your home sits above the base flood elevation. Each foot can mean significant savings.

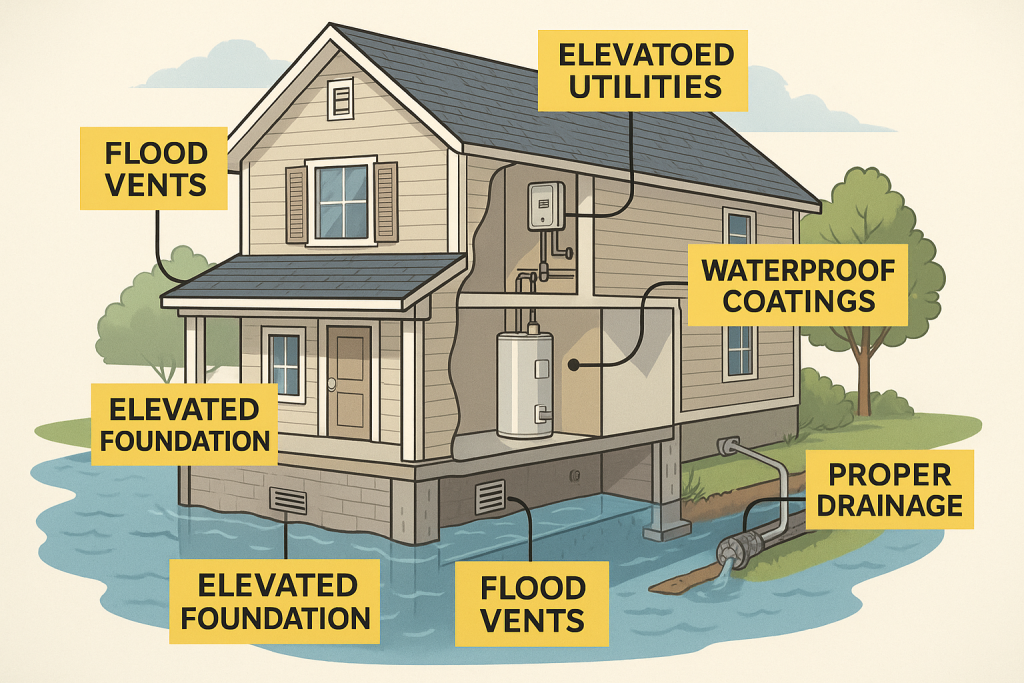

2. Implement Flood Mitigation Measures

Your home’s physical characteristics directly impact your flood risk—and your premium. Consider these proven mitigation strategies:

- Elevate utilities: Moving your HVAC system, water heater, and electrical panels above the base flood elevation can reduce potential damage and lower premiums.

- Install flood vents: These specialized openings allow floodwater to flow through enclosed areas rather than pushing against your walls. They’re particularly effective for crawlspaces and garages.

- Create proper drainage: French drains, sump pumps, and properly graded landscaping can direct water away from your foundation.

- Apply waterproof coatings: Specially designed sealants can protect your foundation and lower walls from water intrusion.

These improvements aren’t just theoretical—they translate to real premium reductions. For example, elevating utilities above the base flood elevation can reduce premiums by 5-15%, depending on your insurer.

3. Challenge Your Flood Zone Designation

When FEMA flood map zoning changes misclassify your property, you have the right to appeal through a process called a Letter of Map Amendment (LOMA) or Letter of Map Revision Based on Fill (LOMR-F).

This isn’t just bureaucratic wishful thinking—it works. According to FEMA’s own data, nearly 83% of LOMA applications are approved, resulting in properties being removed from high-risk designations.

The process requires specific documentation, including: * Your elevation certificate * Property deed or tax assessment * FIRMette (portion of the flood map showing your property) * Completed MT-EZ or MT-1 form

While the process typically takes 30-60 days, the potential savings make it worthwhile. The Richardsons in Texas successfully challenged their new Zone A designation with a LOMA, saving over $1,200 annually on premiums.

4. Leverage Community-Based Solutions

Your individual efforts matter, but community-wide approaches can be even more effective. FEMA’s Community Rating System (CRS) rewards entire communities that implement flood mitigation measures with discounted insurance rates for all residents.

These discounts range from 5% to 45%, depending on the community’s classification. Currently, over 1,500 communities participate, benefiting millions of policyholders.

How can you help? Advocate for your community to: * Join the CRS program if it hasn’t already * Improve stormwater management * Preserve open spaces in flood-prone areas * Enhance emergency notification systems * Develop stricter building codes for flood resilience

Community action creates a multiplier effect—your individual premium decreases while property values throughout the area remain more stable.

5. Explore Grandfathering Options

When FEMA flood map zoning changes increase your risk classification, “grandfathering” provisions may allow you to keep your previous zone rating. This isn’t automatic—you need to be proactive.

There are two main grandfathering approaches:

- Continuous coverage: If you already have a flood policy when maps change, you may be able to maintain your previous rate.

- Built-in-compliance: If your home was built in compliance with the flood map in effect at the time of construction, you may qualify to use that map for rating purposes.

The key is timing. You must secure coverage before the new maps become effective to qualify for continuous coverage grandfathering. This is why staying informed about upcoming FEMA flood map zoning changes is crucial.

6. Consider Private Market Alternatives

The National Flood Insurance Program (NFIP) isn’t your only option anymore. The private flood insurance market has expanded significantly, often offering more competitive rates, especially for properties affected by FEMA flood map zoning changes.

Private insurers typically use more sophisticated models that consider property-specific characteristics rather than relying heavily on FEMA’s zone designations. This can result in lower premiums for many homeowners.

Additionally, private policies often offer: * Higher coverage limits than NFIP’s $250,000 structure/$100,000 contents caps * Shorter waiting periods (typically 14 days versus NFIP’s 30 days) * Additional living expense coverage (not available through NFIP) * More flexible payment options

The savings can be substantial. A recent analysis found that 77% of single-family homes in Florida could find cheaper coverage in the private market than through NFIP.

7. Conduct Annual Policy Reviews

The flood insurance landscape changes constantly. New FEMA flood map zoning changes, policy updates, and private market options emerge regularly. An annual review with a knowledgeable insurance agent can ensure you’re not overpaying.

During this review, discuss: * Any mitigation measures you’ve implemented * Changes to your property * New private market options * Upcoming map revisions * Available discounts and programs

This isn’t just about finding immediate savings—it’s about developing a long-term strategy to manage your flood risk and premium costs.

Navigating the Map Change Process

When FEMA announces new flood maps for your area, you’ll want to understand exactly how the changes affect your property. Here’s a step-by-step approach:

- Check your current and proposed designations: Visit FEMA’s Flood Map Service Center (MSC) at msc.fema.gov to view both current and preliminary maps.

- Understand the timeline: Map revisions follow a specific schedule, including:

- Preliminary map release

- Public comment period (90 days)

- Letter of final determination (6-month notice)

- Effective date

- Attend community meetings: FEMA typically holds public sessions to explain changes and answer questions.

- Consult professionals: Speak with surveyors, engineers, or flood specialists who understand the technical aspects of FEMA flood map zoning changes.

- Prepare your appeal: If you believe the designation is incorrect, gather evidence early.

The success rates for different types of appeals vary significantly:

| Appeal Type | Description | Number Filed | Number Approved | Success Rate | Avg. Processing Time |

| LOMA (Letter of Map Amendment) | For properties incorrectly mapped in SFHA | 42,350 | 35,123 | 82.9% | 60 days |

| LOMR-F (Letter of Map Revision Based on Fill) | For properties elevated by earthen fill | 8,750 | 6,213 | 71.0% | 90 days |

| LOMR (Letter of Map Revision) | For changes in flood hazards, BFEs, etc. | 5,230 | 3,245 | 62.0% | 120 days |

| CLOMR (Conditional Letter of Map Revision) | For proposed projects that would affect flood hazards | 1,875 | 1,031 | 55.0% | 150 days |

Source: FEMA Map Service Center Statistics Report, 2024

As these statistics show, challenging your designation isn’t futile—it’s often successful. But timing is everything. You must file within the designated appeal period to have your case considered.

Future Outlook for Flood Insurance and Mapping

The landscape of flood risk and insurance is evolving rapidly. Understanding these trends can help you prepare for future FEMA flood map zoning changes and their impact on your premium.

Climate change is dramatically altering flood patterns nationwide. Areas previously considered low-risk are experiencing unprecedented flooding, while improved modeling reveals vulnerabilities that older maps missed.

The following table shows projected changes in flood risk by region:

| Region | Current Properties at Risk | Projected Properties at Risk (2050) | % Increase | Estimated Annual Damage Increase |

| Northeast | 4.3 million | 5.9 million | 37.2% | $5.2 billion |

| Southeast | 8.7 million | 12.3 million | 41.4% | $7.8 billion |

| Midwest | 3.1 million | 3.8 million | 22.6% | $3.5 billion |

| Southwest | 2.8 million | 3.5 million | 25.0% | $2.9 billion |

| West Coast | 3.9 million | 5.2 million | 33.3% | $6.1 billion |

| Pacific Northwest | 1.2 million | 1.7 million | 41.7% | $2.3 billion |

Source: First Street Foundation Flood Risk Assessment, 2024

Technological improvements are also transforming how FEMA creates flood maps. LIDAR (Light Detection and Ranging) technology now provides elevation data accurate to within a few inches, while advanced hydrologic models simulate water flow with unprecedented precision.

These improvements mean future FEMA flood map zoning changes will likely be more accurate—but also identify more properties at risk. Preparing now can help you avoid premium shock later.

Legislatively, the program continues to evolve. The NFIP has undergone multiple reforms in recent years, with more likely coming as Congress grapples with the program’s financial sustainability. These changes could affect everything from premium caps to mitigation programs.

Taking Control of Your Flood Insurance Future

FEMA flood map zoning changes may seem like an impersonal bureaucratic process, but their impact on your financial well-being is deeply personal. The good news? You have more control than you might think.

By understanding how these changes affect your premium, implementing mitigation measures, exploring all insurance options, and challenging inaccurate designations, you can protect both your property and your wallet.

Don’t wait for the next map revision to catch you by surprise. Take action now to assess your risk, understand your options, and implement a strategy that works for your specific situation.

Your home is likely your largest investment. Protecting it from flood damage—and from unnecessary insurance costs—is worth the effort. After all, when it comes to FEMA flood map zoning changes, knowledge truly is power.

Frequently Asked Questions About FEMA Flood Map Zoning Changes

How often does FEMA update flood maps?

FEMA aims to review flood maps every 5 years, though actual updates vary by community. Some areas may see revisions more frequently due to significant development or environmental changes, while others might go longer between updates. You can check your community’s status on FEMA’s Map Service Center website.

If my property is newly mapped into a high-risk zone, am I required to buy flood insurance?

If you have a federally backed mortgage, yes. Federal law requires flood insurance for properties in high-risk zones (A or V) with loans from federally regulated or insured lenders. Even without a mortgage requirement, the risk is real—over 30% of flood claims come from properties outside high-risk zones.

How can I find out if my property’s flood zone designation is changing?

FEMA notifies communities, not individual property owners, about map changes. Stay informed by checking with your local floodplain manager, attending community meetings about flood map updates, or regularly visiting FEMA’s Map Service Center website to view preliminary maps for your area.

Can I get flood insurance if my property isn’t in a high-risk zone?

Absolutely. In fact, it’s often significantly cheaper to insure properties in moderate to low-risk zones, with Preferred Risk Policies available at substantial discounts. Given that over 20% of flood claims come from these lower-risk areas, this coverage provides valuable protection at a reasonable cost.

How long does the LOMA process take, and what are my chances of success?

The LOMA process typically takes 30-60 days from submission to determination. Success rates are surprisingly high—about 83% of LOMA applications result in properties being removed from high-risk designations. The key is providing accurate elevation data that clearly shows your property sits above the base flood elevation.

If I implement flood mitigation measures, how quickly will my premium decrease?

Premium reductions from mitigation measures typically take effect at your next policy renewal after documentation is submitted. The amount of reduction varies based on the specific measures implemented and your insurer’s rating structure. Some improvements, like elevating utilities or installing flood vents, can reduce premiums by 5-15% immediately.

References and Resources

Throughout this article, we’ve referenced several authoritative sources to provide you with accurate, up-to-date information about FEMA flood map zoning changes and their impact on your premium. Here are the key resources we’ve cited:

- FEMA Flood Map Service Center – The official source for flood hazard information

- FloodSmart.gov – The official website of the National Flood Insurance Program

- FEMA’s Community Rating System – Information on community-based discount programs

- First Street Foundation – Independent research on flood risk and climate change impacts

- FEMA’s Map Changes and Flood Insurance – Official guidance on map revisions and insurance implications

These resources provide valuable information for property owners navigating the complexities of flood insurance and FEMA flood map zoning changes.